Blog

What are Sustainable Financial Disclosure Regulations? | Rio

Copyright Qontigo.com

With headlines at the beginning of this year stating that global ESG assets may surpass $41 trillion by the end of this year and $50 trillion by 2025,1 none can argue that ESG investing has gained unprecedented traction.

As Environmental, Social, and Governance (ESG) factors increasingly become part of investing conversations, there’s an influx of new information and scrutiny which is going play an important role as regulators tackle the risk of greenwashing.

Sustainability data has increased in volume and, as a result, ESG investments are rising to the top amidst increases in regulations. But there remains a big barrier for investors who want to take the leap: the unavailability or lack of transparency of data.

The fact is that definitions and methodologies around concepts such as ESG, impact and sustainability have been vague, providing room for investors to infer their own expectations or interpretations.

In this blog, we look at what the EU Sustainable Finance Disclosure Regulation's mean, who they affect and what they entail.

Source:https://go.factset.com/hubfs/Website/Resources%20Section/Brochures/sfdr-disclosing-principal-adverse-impact-indicators-brochure.pdf

Source:https://go.factset.com/hubfs/Website/Resources%20Section/Brochures/sfdr-disclosing-principal-adverse-impact-indicators-brochure.pdf

What is the EU Sustainable Finance Disclosure Regulation?

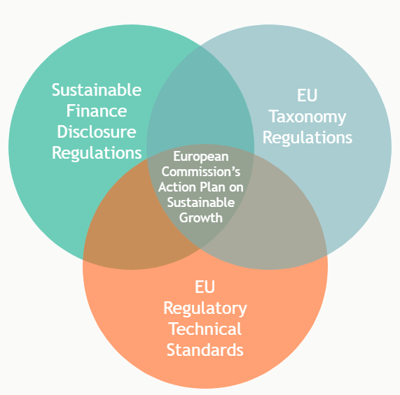

The Sustainable Finance Disclosure Regulation (SFDR), which was introduced in 2019 and came into effect in March 2021, is part of a new wave of European regulation aimed at building a sustainable economy.

Since 2017, the European Union (EU) has been strengthening its sustainable finance regulation in recognition of the role the financial sector can play in achieving the EU’s sustainable development objectives. The goal of these legislative efforts is to encourage the financial sector to support sustainable activities and to rotate capital away from harmful ones.

The SFDR has been introduced to improve transparency in the market for sustainable investment products, which helps to prevent greenwashing as well as to directing capital towards more sustainable investments/ products and businesses.

The SFDR, together with a range of other EU sustainable finance initiatives, is intended to support the European Green Deal, which envisions a European economy that is both climate neutral by 2050 and positive for biodiversity.

To achieve this, the SFDR focuses on disclosures. There is a general belief that enabling end-investors to better understand the impact their investments have on society and the environment through increased transparency will encourage them to shift capital toward activities that are less harmful and, potentially, even positive.

However, there are two roadblocks to achieving this:

- Sustainable products: Sustainable investment products are products that integrate sustainability or environmental, social, and governance (ESG) considerations.

- Sustainability disclosures: The European Commission (EC) argues that, historically, sustainability disclosures for end-investors, including pension fund trustees, beneficiaries, and retail investors, have been insufficient.2

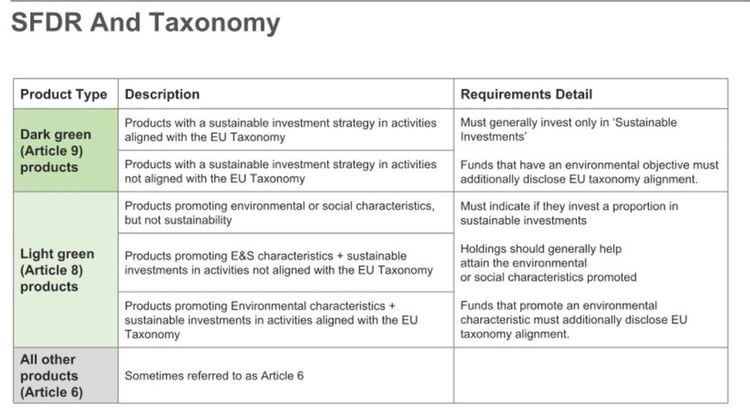

The SFDR classifies funds as grey, light green, or dark green, with stricter reporting requirements for green funds. Investment managers, from the end of 2022, will have to begin reporting on the regulations put in place to ensure companies comply with global standards such as the UN Guiding Principles on Business and Human Rights.

Source: Morningstar

Who does SFDR apply to?

The regulation applies to all Financial Market Participants (“FMPs”) and Financial Advisors (“FAs”) in the EU, FMPs with EU shareholders, and those marketing themselves in the EU, and sets out clear disclosure requirements.

FMPs include:

- An insurance company that makes available an insurance-based investment product

- Investment firms that provide portfolio management

- An institution for occupational retirement provision

- A manufacturer of pension products

- An alternative investment fund manager

- A pan-European personal pension product provider

- manager of a qualifying venture capital fund

- A manager of a qualifying social entrepreneurship fund

- A management company for UCITS (Undertakings for the Collective Investments in Transferable Securities)

- A credit institution that provides portfolio management

The products that it encompasses include (not exhaustive): investment and mutual funds, UCITS, insurance-based investment products, private and occupational pensions and insurance and investment advice.3

To give a sense of the significance of SFDR and why it is important to ensure it is being applied appropriately, according to Morningstar, as of 31 March 2022, 31.5% of funds available for sale in the EU were classified as either Article 8 (27.9%) or Article 9 (3.6%). This definition excludes money market funds, funds of funds and feeder funds.

In terms of assets, the two fund groups account for an even larger share of the EU pie at 45.6% of assets. Article 8 products account for a sizeable 40.7% of assets with Article 9 products accounting for a further 4.9%; the combined assets amount to €4.18trn.4

What is SFDR level 1 and 2?

In April 2022, the European Commission published the proposed Regulatory Technical Standards (RTS) for more information and guidance on the SFDR. There are two levels to the SFDR: level 1 and level 2.

SFDR level 1 disclosures are entity level disclosures which require information about Financial Market Participants (FMP) policies on the identification and prioritisation of principal adverse sustainability impacts. The regulation “requires financial institutions within the EU to make principles-based disclosures on ESG-related activity”, according to IQ-EQ5. This means that firms and companies must report both on the sectors they are investing in and their portfolio companies.

These SFDR disclosures have some requirements too: they are made public on the institutions’ websites, accompanied by a sustainability risk policy.

Level 1 SFDR does not disclose the technical detail on what must be disclosed but is more general by mandating draft RTS to be more specific with the content of the disclosures.

One of the more significant impacts of the SFDR is its mandated disclosure of Principal Adverse Impact (PAI) indicators.

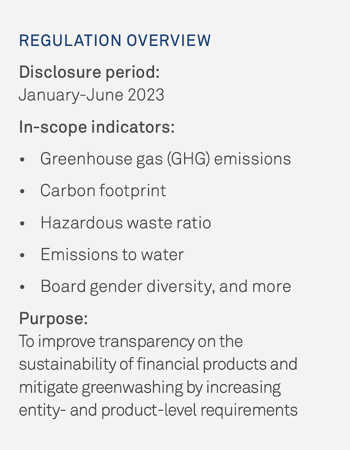

SFDR Level 2 still requires companies to report on 18 mandatory Principle Adverse Impact Statements (PAIS) of investment decisions at legal entity level by 30 June 2023 in respect of a reference period running from 1 January 2022 to 31 December 2022.

The Principal Adverse Impacts (PAIS) must include at least the following:

- Information about their policies on the identification and prioritisation of principal adverse sustainability impacts and indicators.

- A description of the principal adverse sustainability impacts and of any actions taken or, where relevant, planned.

- Brief summaries of engagement policies in accordance with the Shareholder Rights Directive, where applicable.

- A reference to their adherence to responsible business conduct codes and internationally recognised standards for due diligence and reporting and, where relevant, the degree of their alignment with the objectives of the Paris Agreement.6

Timeline for SFDR Level 2

Jan. 2022: Taxonomy statement

Jan. 2023: Application date for SFDR RTS (incl. SFDR reporting requirements for products according to Art. 8/9 SFDR)

Jun 2023: PAI disclosure for reporting period 1 January 2022 to 31 December 2022

Articles 6, 7, 8 and 9 of the SFDR

The SFDR aims to create a more transparent field during investments. With asset managers having to disclose the different levels of sustainability integration, the SFDR is categorised into articles. The main ones are Articles 6, 7, 8 and 9.

These articles impose comprehensive sustainability disclosure requirements covering a broad range of environmental, social & governance (ESG) metrics at both entity and product-level.

Article 6 of the SFDR relates to funds which do not take into consideration any sustainability in the investment process and could include stocks which are not included by ESG funds (e.g., tobacco companies). These products will still be sold in the EU, but they need to be labelled as non-sustainable.

This Article – Integration of sustainability risks in investment decisions – has some pre-contractual disclosures:

If sustainability risks are integrated into the investment decision-making process, the asset manager has to disclose how they are integrated.

If sustainability risks are not integrated, the asset manager must explain why.

Article 7 revolves around accessing the adverse impact investment decisions have on sustainability. There are additional pre-contractual disclosures on each investment portfolio, which state that the asset manager has to consider all the adverse impacts that the investment has on the sustainability factors. Article 7 will come into force on 30 December 2022.

From December 2022, the manager must be transparent about any negative impacts on sustainability and why. The question that must be asked is: “Does this financial product consider principal adverse impacts (PAI) on sustainability factors?”

Also known as environmental and social promoting, Article 8 covers financial products that are characterised by environmental and social factors, and whether their companies have good governance practices.

ESG investing is not the core factor of these products. Article 8 states that the disclosed information has to explain how these requirements are met.

Article 8 funds are categorised as light green.

Article 9 funds are classified as dark green.

Under SFDR, an Article 9 fund is described as “a Fund that has sustainable investment as its objective or a reduction in carbon emissions as its objective”. There are requirements that must exist for the fund to be considered sustainable:

The fund must incorporate good governance into the investment strategy.

Article 9 relates to the fund portfolio, establishing whether or not the financial object causes any significant harm.

Article 9 funds with a carbon reduction aim must refer to an EU Climate Transition Benchmark or an EU Paris-aligned Benchmark.8

Source: https://www.anthesisgroup.com/a-guide-to-the-eu-sustainable-finance-disclosure-regulation/

In summary

The SFDR is designed to help institutional asset owners and retail clients understand, compare, and monitor the sustainability characteristics of investment funds by standardizing sustainability disclosures.

The SFDR classifies funds as grey, light green or dark green, with stricter reporting requirements in place for the green funds.

Under the SFDR, firms must make both firm and product-level disclosures about the integration of sustainability risks, the consideration of adverse sustainability impacts, the promotion of environmental or social factors, and sustainable investment objectives.

The solution is in powerful reporting.

How can we help?

Rio is an intelligent sustainability software platform that helps you improve your impact on the planet, manage ESG risk, and save money.

Data is driving the revolution of sustainable investing. By centralising ESG data, Rio helps financial service providers gain unprecedented visibility into the ESG performance of their portfolio and conduct ESG due diligence on investment targets.

Rio takes the guesswork out of comparing datasets to allow for more sound financial investments. The more data we can effectively measure, the more improvements we can make—and the more investments can go to supporting the best practice sustainability efforts.

Rio also enables reporting in line with a wide range of ESG disclosure requirements and legislation such as the SFDR, EU Taxonomy and TCFD.

Download our guide on ESG Due Diligence, Compliance, and Voluntary Reporting: A Data Collection Guide for Financial Services.

2 https://www.intuition.com/what-is-the-sfdr-sustainable-finance-disclosure-regulation/

3 https://www.anthesisgroup.com/a-guide-to-the-eu-sustainable-finance-disclosure-regulation/

4 https://capitalmonitor.ai/regions/europe/explainer-what-are-the-sfdr-regulations/

5 https://iqeq.com/insights/are-you-ready-meet-sfdr-annual-reporting-requirements

7 https://capitalmonitor.ai/regions/europe/explainer-what-are-the-sfdr-regulations/

8 https://www.cfainstitute.org/en/research/esg-investing

Check out other articles

Embracing Double Materiality

3 October, 2024 Environmental Law and Compliance,

Blog

Six reasons to be optimistic about the climate summit.

8 November, 2022 / Environmental Law and Compliance, Carbon, Climate Change, cop27,

Blog